A method for management to demonstrate the existence and effectiveness of its internal financial controls. This documentation can be in the shape of a Standard Operating Procedure (SOP), Process flow chart, narratives, excel sheets containing risk control matrixes and so on.

Many organizations adopt the ‘control catalogue approach’ ie specify certain minimum expectations on its internal control environment. A ‘control catalogue’ contains – control objective, control activity, control frequency and organization policy & procedures are often referenced, wherever possible.

You must be reminded that expecting a 100% compliance is a recipe for failure.

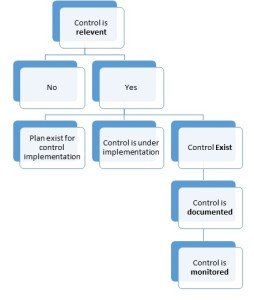

With the basics of Control Self-assessment in place, the various operating units are asked to self-assess their control environment. This assessment requires the various process owners to answer questions in simple ‘Yes / No / NA’. Once an assessment is completed, a summary of control environment maturity is developed.

I welcome your inputs on above.